A version of this article first appeared in the July Executive Report: Keeping pace with the payments evolution. Check out the full issue for insight from banking thought leaders who examine consumer and business trends driving faster adoption of the many new ways to transact. Plus, we address key industry considerations that come with these changes.

While most financial institution executives consider faster payments a “must have,” quite a few still perceive significant hurdles stymying full adoption. Two of the biggest factors getting in their way are chalked up to what their counterparts on the solutions side believe are misperceptions: challenges with interoperability and the potential for widespread fraud.

At least that’s a bit of the sentiment gleaned from the 2025 Faster Payments Barometer, a survey of more than 400 executives at FIs, other businesses, associations and technology providers released by the U.S. Faster Payments Council, in collaboration with Volante Technologies, which is based in Jersey City, N.J.

The concerns are real. They’re also not ignored. Addressing the pain points head on and with right-sized, versatile and secure solutions may not be as far off as many institutions believe.

Volante’s Deepak Gupta sat down with BAI to make the case that there’s a disconnect between perceived challenges and reality. Gupta, who’s also an advising board member of the Faster Payments Council, shared some of the key findings of this year’s survey, and what it will take to get more traditional banks and credit unions on board with faster payments.

What are the Barometer’s key takeaways?

There are a few key messages. Although [payment rails] The Clearing House’s RTP has been in production for roughly eight years now and FedNow for almost two years, there’s still a long tail of financial institutions waiting to fully utilize RTP and FedNow.

Only 22% of the institutions currently connected to either RTP or FedNow are small and medium-sized institutions that can process both send and receive payments. While a lot of them can receive, it’s only if another party sends them first. There’s also a large number of institutions that still haven’t adopted either one or both payment networks.

Moreover, only 61% of the survey respondents feel that satisfactory progress towards instant payment adoption is being made. This shows that not only is there a long tail, but there’s also a little bit of frustration over the slow start to the process.

Having said that, there are some promising signs. Of the institutions that are trying to implement faster payments, almost 90% of the planned projects are for the next two years. While there may be a long tail it’s catching up quickly. I think over the next two years you will see a very broad and massive adoption of faster payments.

The long tail and the slowness are due to many reasons. It takes a long time and it’s expensive to implement a new payment type. But with the advent of Payments-as-a-Service (PaaS), institutions can go live in less than three months. It’s not complex, expensive, difficult or risky anymore to implement a new payment type — and it’s not hard to integrate with other payment types.

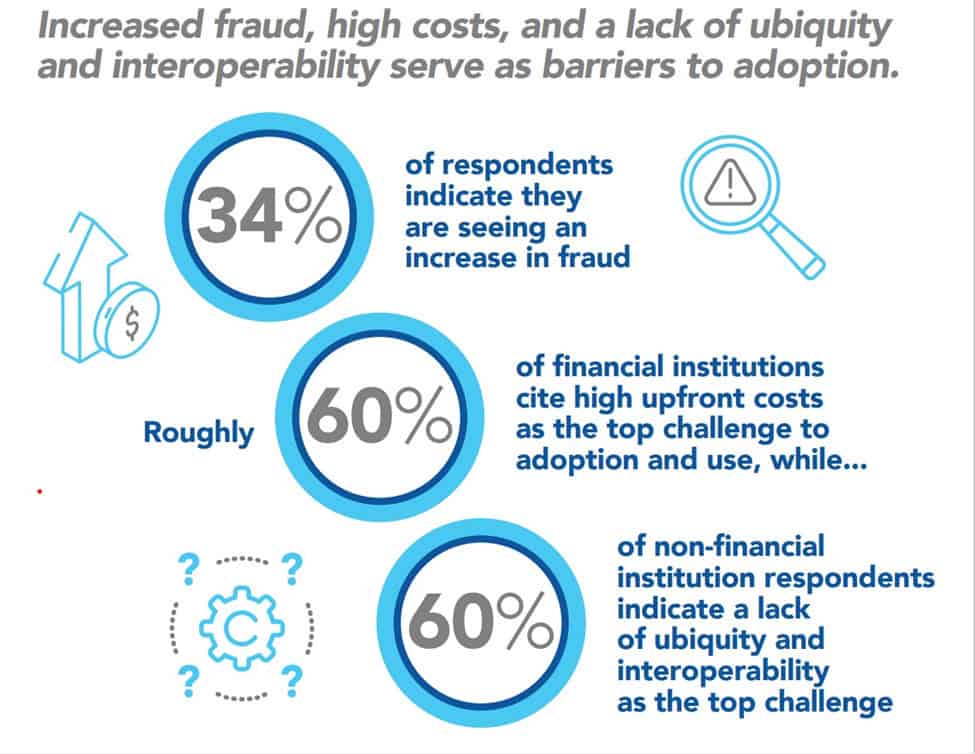

Another key finding from the survey is that fraud continues to be a concern across the board. Institutions, speaking broadly, are slow to commercialize faster payments because of the mere perception of fraud, but some of it is reality as well. While these are smaller-value payments on the rails, there are larger numbers of transactions, so an increase in fraud is likely to happen.

Having said that, only 3% of the respondents said that this is a significant risk. As you can see, it’s a double-edged sword. Respondents think it’s a major concern, but at the same time, they don’t think it’s a significant risk.

I think that adoption of faster payments is inhibited by the fact that most smaller institutions don’t have 24×7 fraud departments. Usually, they have a fraud department working eight to 10 hours, and automated fraud systems that are available 24 hours a day. But even if the system flags something as fraud, it requires a human to review it. So far, I don’t think institutions have seen the demand to be able to make that kind of investment in the people and resources to be truly 24×7.

A majority of U.S. banking executives said they’ve been slower to jump on real-time payment rails because of cost and because operations and transaction messaging won’t be uniform, although that has changed with ISO 20022 implementation. They’re also concerned about payments fraud, although less so. These are the top findings in a survey conducted this year from the U.S. Faster Payments Council and Volante Technologies.

The third reason for the slowness of payments adoption is there’s a big discrepancy between faster payments use cases that institutions are planning to invest in versus what the business community wants. For example, over half of business owners are very interested in point-of-sale and e-commerce. Business owners also want to use faster payments for invoicing and supply payments. Yet only 16% of institutions are planning to provide these services. In time, you will see more and more use cases being offered by institutions to businesses.

Let’s drill down on technical aspects of implementation.

If you think about the payment systems of the past, they needed to be very mainframe-centric systems. They were old, they didn’t scale well, and they weren’t flexible. Institutions weren’t able to customize because the resources that built those systems have since retired. So, it’s not only expensive, but it’s also difficult to maintain these existing payment systems.

As such, institutions have started to modernize their systems. Due to ISO 20022 compliance, more institutions have taken the opportunity to modernize Fedwire. ACH will be the next one to fall, and the same trend applies in other parts of the payments world.

Share your thoughts on interoperability.

Interoperability happens at two levels. One is the simple interoperability between FedNow and RTP, but that’s not a showstopper at all. What businesses really care about is the ability to process both FedNow and RTP, automating which payments go to FedNow and which payments go to RTP. This is available, for example, by implementing a third-party PaaS system.

In our annual survey, the concern around interoperability has been reduced from 78% to 61% over the past five years. What’s more important is for institutions to start looking at what they do to provide value-added services over and above just instant payment services. This includes invoicing, account receivables and e-commerce.

Why are institutions using both rails?

I think multi-rail applies to more than RTP and FedNow. Multi-rail is a new concept where vendors like Volante and others are offering a payments hub as a solution. This allows us to offer multiple payment types within a single solution.

In the past, institutions implemented different solutions from different vendors for every separate payment type. Now, institutions prefer to have a single solution that can handle multiple different payment types. They’re focused on being able to offer more services to their customers, providing them in a more efficient way.

Interoperability at the payments level is called smart routing, which can be done depending on the conditions and rules defined by a bank, and then the payment is sent not only to RTP or FedNow, but also to a wire or an ACH.

This is beneficial for an institution because it’s a one-stop option, it lowers the risk, and it lowers the complexity of working with multiple vendors and multiple contracts.

It also makes it easier to monitor the application, because one application for all payment types allows for smart routing, as well as for institutions to modernize their payments systems at their own pace. So, they don’t have to do a Big Bang approach — they can add payment types in steps.

Is multi-rail demand also a byproduct of a deep U.S. banking system with so many participants and layers?

It’s not specific to the U.S. — there are only a few payment types which are applicable to any region in the world. The older ones are low value, like ACH payments for payroll, and high-value payments are wires. Now, instant payments has become a cross between the low value and high value, due to the RTP cap having risen to $10 million.

There are new payment types coming, such as crypto, more digital assets, and other P2P payment types, that are not just a function of the U.S. The complexity arose due to the absence of a vendor with a payment hub approach, so it was a best-of-breed solution. While that sounds very good, it’s a nightmare to integrate with multiple parties. So, the best-of-breed is now taking a back seat, and the payment hub solution with multiple payment types is the new way forward.

You’ve told us about potentially nightmarish upgrades of legacy systems — why are third-party solutions often the better route?

More and more institutions have started to ask for an out-of-the-box solution for payment types like wires, because they’ve become a commodity and customization isn’t required — which means it’s easier to maintain and upgrade.

Additionally, payment volumes are increasing dramatically, more than legacy systems can handle — meaning that institutions are now modernizing their payment systems to be able to say yes to their business customers. They are also modernizing to be more flexible and resilient as they make more changes and as new rules come out every year, including going to the ISO 20022 format.

Some vendors offer a payment solution in a Software-as-a-Service (SaaS) model, where a bank doesn’t have to have the expertise, the resources or the hardware — or even the software onsite. A SaaS model might integrate with a home-grown fraud application, core banking application, or any other applications. Or modernize an institution’s ACH platform to help in migration from any legacy platform they have on ACH.

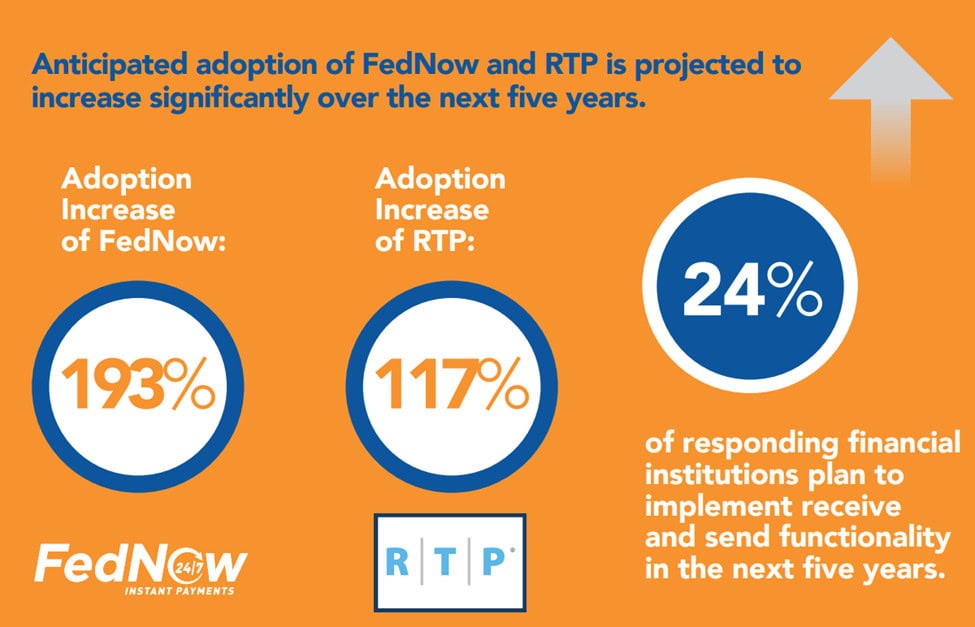

The 2025 Faster Payments Barometer asked U.S. banking executives to forecast their likely usage of “receive” and “send” payment functionality in the next five years on both the Federal Reserve’s FedNow instant payments platform and banking consortium The Clearing House’s RTP platform. To date, real-time payments offerings at some U.S. financial institutions had been limited to receive only, which had slowed the expansion of the ecosystem.

What else is important for banks and credit unions to consider?

One of the approaches we recommend is to use an embedded payment processing solution — a single system where all payments are processed and subsequently coordinated so that the payments flow to their different legacy systems. Once an institution implements this system, they can slowly replace each legacy system, one payment type at a time.

The second thing institutions must consider is beyond payment processing. Think about how to leverage new data types to offer services around that data. How can they provide new intelligence to customers leveraging that data? How do they use AI to analyze data and predict trends for customers?

The data, for instance, might live on the top of the payment hub. It leverages AI to analyze the ISO data points on transactions within the hub to predict trends to institutions, including dollar volumes, payment volumes, resiliency, quality of service and more.

If you’re a financial institution and your customers demand new services very quickly – they don’t even want to wait for three months. If you are not able to help your customers now, you are going to lose them. That’s why modernization is a must, not optional.

Katie Kuehner-Hebert is a contributor to BAI.